The Week Ahead

Volume 131 - The real signal is not de-escalation. it’s disarray

Last week offered one of the most violent re-risking (cover bid) episodes since the Global Financial Crisis, yet the underlying market structure remains impaired. The S&P 500 rallied nearly 10% off its lows, while the NASDAQ surged more than 12%. Volatility crushed (though VIX still remains above 30 and VVIX above 140), hedge funds covered their positions, and long-only investors chased performance.

However, the fundamental backdrop remains one of unresolved uncertainty. The supposed "Trump pivot" appears less a signal of policy clarity and more a desperate effort to re-anchor risk. This was not a resolution in my opinion - it was a reflex and a moment of panic.

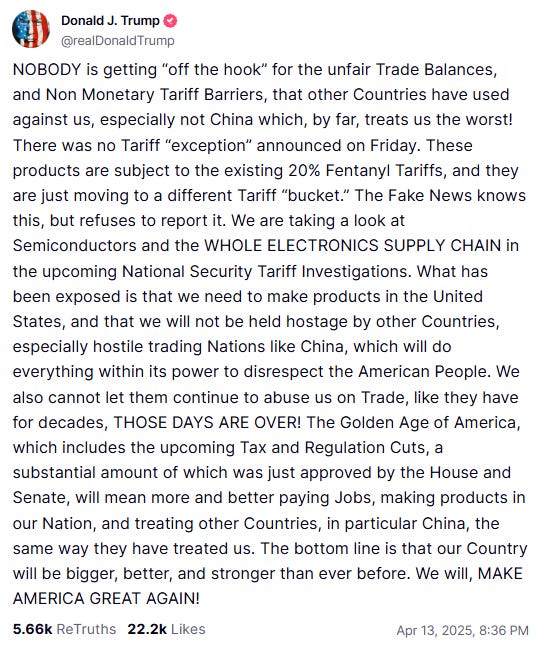

Market participants were handed what looked like a dovish inflection point- the White House walking back its tariff policy through:

A 90-day pause on reciprocal rates (excluding China)

A partial exemption for consumer electronics

Notably, the latter announcement didn't come through Trump's Truth Social account but quietly via the Customs and Border Protection website.

Despite last week's price action, there's been no structural improvement in the core issues:

Tariffs on China remain at punitive levels

Supply chain visibility is deteriorating

Any perceived policy easing appears transitory

Earnings visibility remains poor, and the macro picture shows no improvement. The notion that a single-week relief rally invalidates the broader market fragility is simply lazy thinking. If anything, it reinforces the idea that there is no coherent framework for trade policy - just reactive improvisation designed to calm markets temporarily rather than provide actual guidance.

Liquidity remains problematic. On April 7th, the bid-ask spread for the median S&P 500 stock jumped to 22bps (the highest since March 2020). Top-of-book depth on S&P actually ticked below $1mm during the week. These are not healthy internals. They are the artefacts of deleveraging and dysfunction. In that context, the scale of the bounce should be understood as a mechanical unwind aided by a lack of liquidity, not an expression of investor conviction.

From a flow perspective, the story is consistent across different desks: Wednesday's reversal was dominated by ETF inflows, covering of index shorts, and a scramble by LOs to re-enter Tech and AI names they had just sold. Prime book data shows discretionary hedge funds were net buyers of US equities last week, while gross leverage in L/S funds rose by 2.2pts to 202.7%. Yet net leverage remains pinned near the zero percentile on a five-year basis. These are defensive flows, not aggressive re-risking. Though I am surprised gross is on the rise as I would personally expect further de-grossing.

More broadly, there's still no evidence that hedge fund buying has progressed from covering to net long initiation. ETF volumes accounted for 40% of all tape flow midweek. Skew remains elevated and put-call ratios are still near extremes. The S&P straddle into Thursday's expiry implies a 3% move, hardly a low-vol regime, though that’s lower than what it was trading at on Friday (>4%).