Positioning Looks Like Another Dump Is Coming

Between the Lines - Vol. 5

It’s been two weeks since I last wrote, new son and the market did exactly what it was supposed to.

Let’s do the unseemly thing first…

Last time I wrote, the S&P was in the 6600s, consensus was that the bounce had already gone too far, and I said the path of max pain was 7,200. Spot as I write this is 7165, 7,000 in Q2 was my call. We are past it, and we are past it on the exact set-up I described.

The trades have done the talking while I have been inactive on the writing front (although I do plan to release the Zero to Options Hero post soon)

SPX 6500/7000 risk reversal for 6/18 put on at -18 now marked at 265

SPX 5900P for September sold for just shy of 200, now trade at 65

Phase 2 basket continues to do its job

Phase 3 still a smidge off where I would like it

CRDO (purple cable go brrr) at 6% nearly approaching 200 (I shared this in the mid 40s last year) now a 3% weight after taking some gains off at Friday’s close after reaching the $200 price target.

The list is, frankly, too long to keep going - there’s some pain in the software names I hold, but overall, the book is outperforming, and that’s what matters.

I leaned the right way when CTAs were “max short” and the doomers were lining up for their oof moment. And I also leaned the right way through the lazy “the bounce has been too much too fast” consensus that we saw in the first half of April.

But the trade has changed. The market did what I wanted. Now I'm doing something different. And I think most people are about to give back what they just made even if index keeps trading higher.

The easy thing to do here is say the market is crowded, index is high and that we should all sell everything since the market has done what I wanted to do. This is not what I think and crowded is totally the wrong word.

Index has caught up to the set-up but everything underneath hasn’t become one giant consensus long which matters as this is where people get lazy. They look at spot, see 7100s and decide the market must be euphoric, and then miss the fact that there is still a tonne of stress and disagreement under the surface.

It may not be the same setup as a month ago, but it is also not some beautiful everyone is all in top. It’s way more awkward than that…

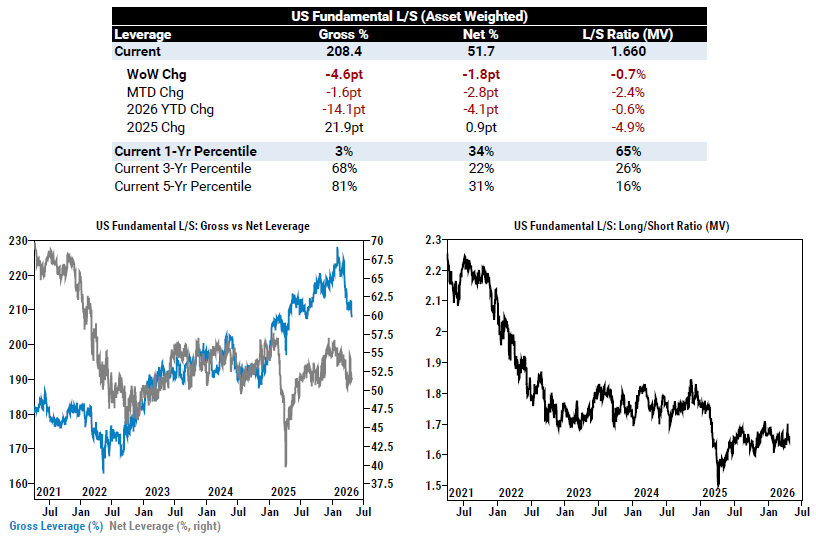

Prime data continues to show the strangest combinations you can get. Index at the highs, AI leadership broadening, earnings coming through better than expected and yet US L/S books have just seen the largest notional de-grossing in seven months. Gross down hard, net down too and single stocks the centre of the unwind. Tech saw one of its largest weekly de-grossing episodes in years, while consumer discretionary was sold by HFs for the seventh straight week.

The above is not what euphoric participation looks like… it is when the market is doing one thing and the average PM is still fighting a war inside their book. It is hard to be bearish seeing this positioning.

The CTA/systematic bid that helped drive a lot of this has done real work. Rough estimate from banks is that the systematic community has bought ~200B of global equities MTD, taking positioning from a 2 to 6. They were short, trend flipped, vol calmed down enough and they simply HAD to buy. From here the baseline flow picture looks more neutral though they will add exposure if rVol continues on a downward trajectory and we continue trending higher.

This does mean that you can’t rely on the same argument here though. At the lows, the argument was very simple. People were too hedged, too bearish, too underweight… the same when the market bounced but then others started to get convinced that the bounce had gone too far. This was all enough for the market to rip. Didn’t even need every stock to perform well nor every headline to smell like roses - just needed price to stop falling and positioning to be wrong. So now the systematic positioning argument is slightly less clean.

The market can absolutely go higher from here, a lot higher… But the next leg needs more than everyone is the wrong side of the boat/offside. The sloppy bear case has been embarrassed and the same people who thought 6900 was impossible are now trying to work out whether 7300 in Q2 is conservative.

I think the thing I care most about here is not whether the S&P can print a higher number as of course it can. The thing I care about is whether the next dollar of risk belongs in the same place as the last one, which I don’t think it does. The market seems to be moving from beta recovery to leadership discrimination. The rally started off as a positioning squeeze, and leadership is not really Mag7 anymore. Mag7 breaking out does matter, sure, but the more important thing is what is happening underneath the index. The AI trade is no longer owning the obvious mega-caps and sleep as we have seen for a while now. The market is continuing to reprice the entire stack behind AI - semis, optical, data centres, inference beneficiaries and so on.

The boring stuff is becoming less boring because the bottleneck keeps moving and that is the bit that most people still don’t get. AI was once a GPU story, then a data-centre story, then a power story and now it is a full-stack infra story… (soon I hope a software story). Markets are paying for everything required to make the models useful, scalable, cheap/fast/available enough which is why Phase 2 worked so well as it covered all angles. Like CRDO, a bottleneck with a ticker. I guess the annoying thing about AI as a theme in general is that once everyone learns the lesson of bottlenecks getting paid, the obvious bottlenecks get expensive very quickly, and if you’re late, you become the momo guy you didn’t want to be.

I think you need to respect price, CRDO on Friday was a pure example… While I can see the name eventually trading at a 300 handle, my cut was not me losing conviction but respecting price and my target.

I still like the AI infra complex as I think the direction of travel is clear. I would argue that the market is underestimating how large the physical economy around AI can become, but saying this, I am much more interested now in what has not been fully repriced higher than in chasing the bits that have already become everyone’s favourite chart.

I think the next layer is probably power flexibility. For the last year, the market has been obsessed with whether there is enough power for AI which was totally the right question. Data centres need power and grids are constrained and time to power has become one of the biggest bottlenecks in the buildout. The next problem isn’t just total capacity but the shape of demand as training is heavy. Inference is real time, user facing and much spikier. As AI gets embedded into actual workflows and agents, the power requirement becomes less smooth and more volatile which changes things. The question goes from who can produce more electricity and becomes who can deliver flexibility into a system that was never built for this kind of load. Which is why energy storage is starting to matter a lot. Storage will smooth the spikes and reduce peak load pressures + defer infra spend. Electricity as inventory is a very big idea if compute demand is moving towards real-time.

Read a good document at the weekend on it from Morgan Stanley, who have Power for AI as a $1.5T theme rotating from capacity into flexibility. They estimate that data centre linked ESS (energy storage system) deployment could reach ~321GWh by 2030, which is roughly the size of the entire global utility scale ESS market. Sodium-ion could reset costs lower over time which would make storage economic across more use cases. Don’t really want to turn this into a newsletter about batteries but this is one of the spots where the AI trade is evolving. By all means, this does not mean whatsoever to buy every energy storage name with both hands as a lot of them are junk and will dilute you into a coma. But the theme is real, and this is exactly the kind of thing I want in my book when the market starts moving toward finding third-order beneficiaries. Which is why I am also not giving up on Phase 3/software. The trade has been painful, and there’s no point dressing it up. Software vs semis has been horrific and the unwind is going to be nothing short of incredible when people realise that software isn’t going to die. The AI kills software thing is just lazy and the market is rewarding picks and shovels still because the capex is visible. Customer lock-ins are not going to diappear just because some anonymous account on Twitter discovered agents… Owning the highest beta bad software just because it's down is equally lazy. So there are lots of names out there to find and lots of problems to solve. Just need to add more exposure to software where AI becomes a feature, a distribution advantage or a workflow expansion tool.

The other squeeze mechanic that I think people are still underestimating is the short-call/overwrite universe. There is a lot of money in products that have effectively been selling upside because everyone wanted equity income with less bond pain. That works until the market starts ripping through the strikes. Then they are not just passive sellers of vol anymore. They have to cover, roll, adjust, and in some cases buy back upside into a market already making highs. It is another reason why spot up can become vol up, and why waiting patiently for a nice little pullback can become an expensive hobby. The market does not need everyone to be bullish when enough people are structurally short the right tail.

This brings me to the macro left tail. I think we can all agree that the market has done a great job at looking through Iran, Hormuz, oil pricing and rates repricing. The market is probably right to see through the noise and turn its focus onto earnings and capex. But there is a difference between looking through something and pretending it doesn’t exist which is why I still want to own a bit more downside. The Strait situation is not clear at all and crude supply disruption hasn’t shown up in finished product shortages yet. The market has turned from war macro to earnings micro in a matter of weeks and while that can last, it could also reverse extremely quickly if oil, freight and input costs start hitting the wrong parts of the economy.

The safest thing to do is avoid parts of the market that are exposed to higher oil, stickier inflation and a squeezed real income consumer (despite me thinking inflation doesn’t stick). Cheap is not a catalyst, lagging is not a thesis nor is pain automatically an opportunity.

So where does this leave index I ask myself? Higher.

Not in a straight line and without stupid air pockets, not without a few days where everyone decides the world is ending again because of a 2am headline. But higher. The earnings backdrop is good enough so far, the AI capex impulse is powerful enough, leadership is broadening in the right places, buybacks are supportive, positioning is far from euphoric, and the people who missed the move still have to explain why they are underweight a market making highs. That last bit matters more than people admit. Markets don't need everyone to be bullish to go up. They just need enough people to be wrong. There are still plenty of wrong people. The difference now is that the easy wrong has been punished. The next part will be more selective and more violent within. Some winners will run much further than people expect. Some good stories will stop working because the market has already paid them.

So I will stay constructive and not be lazy like I was in other bull runs. You trim into rips and buy dips. Stay long the right tail and keep looking for the next bottleneck as the path of max pain remains higher if earnings keep doing what they’re doing. Hedge where convexity is cheap and trim where price has done enough. That’s the task now. Here at 7150, the edge is working out what people still don’t own properly, and I think there is enough to broaden this market out and keep it moving a lot higher.